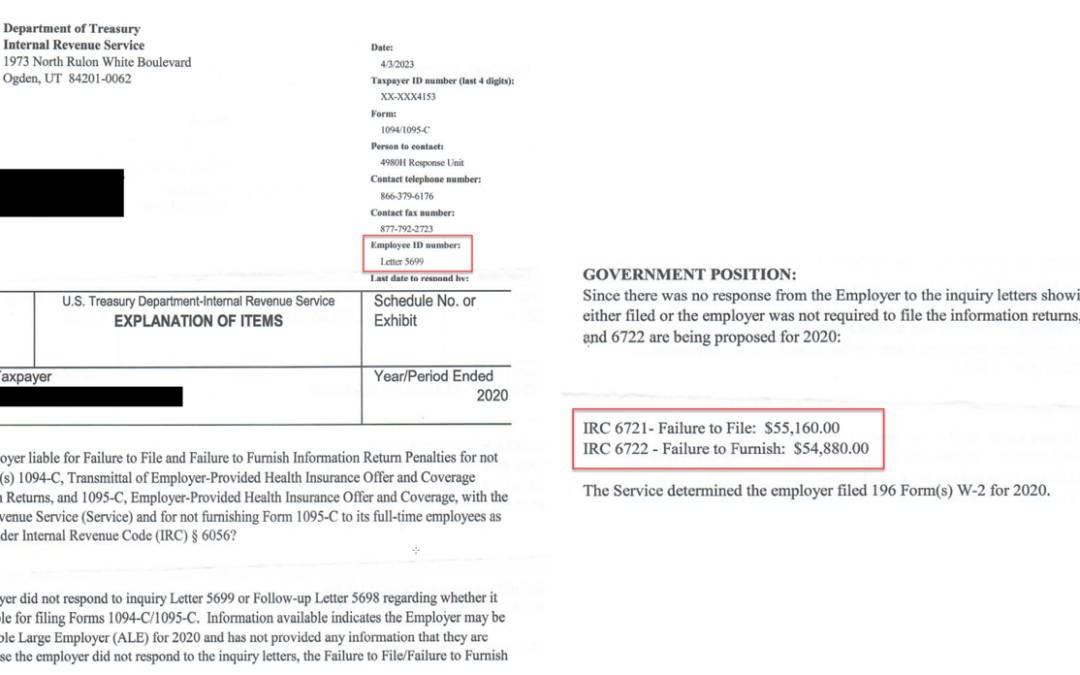

Failure to file or furnish Forms 1094-C and 1095-C as required can result in civil penalties under Code Sections 6721 and 6722, which are indexed each tax year as shown in the table below. These penalties apply separately per form that is not filed or furnished as required.

With the removal of good faith transition relief effective beginning with the 2021 tax year going forward and the expansion of mandatory electronic filing requirements for most filers effective beginning with the 2023 tax year, Employers must ensure they are completing their reporting requirements accurately and timely to avoid these penalties. Haff & Raggio has saved millions for clients hit with these civil penalties through the penalty abatement process with the IRS. If your business needs help, please reach out to appeals@eligibilitytrackingcalculators.com today!

| Tax Year to which the Form relates | General Penalty | Correction within 30 days of due date | Correction after 30th day but on or before August 1st after the due date | Intentionally Neglecting to File or Furnish |

| 2015 | $260 | $50 | $100 | $520 |

| 2016 | $260 | $50 | $100 | $530 |

| 2017 | $260 | $50 | $100 | $530 |

| 2018 | $270 | $50 | $100 | $540 |

| 2019 | $270 | $50 | $110 | $550 |

| 2020 | $280 | $50 | $110 | $560 |

| 2021 | $280 | $50 | $110 | $570 |

| 2022 | $290 | $50 | $110 | $580 |

| 2023 | $310 | $60 | $120 | $630 |

Source: Internal Revenue Manual, Chapter 20.1.7, Exhibits 20.1.7-1 and 20.1.7-2, available at: https://www.irs.gov/irm/part20/irm_20-001-007r